Blog

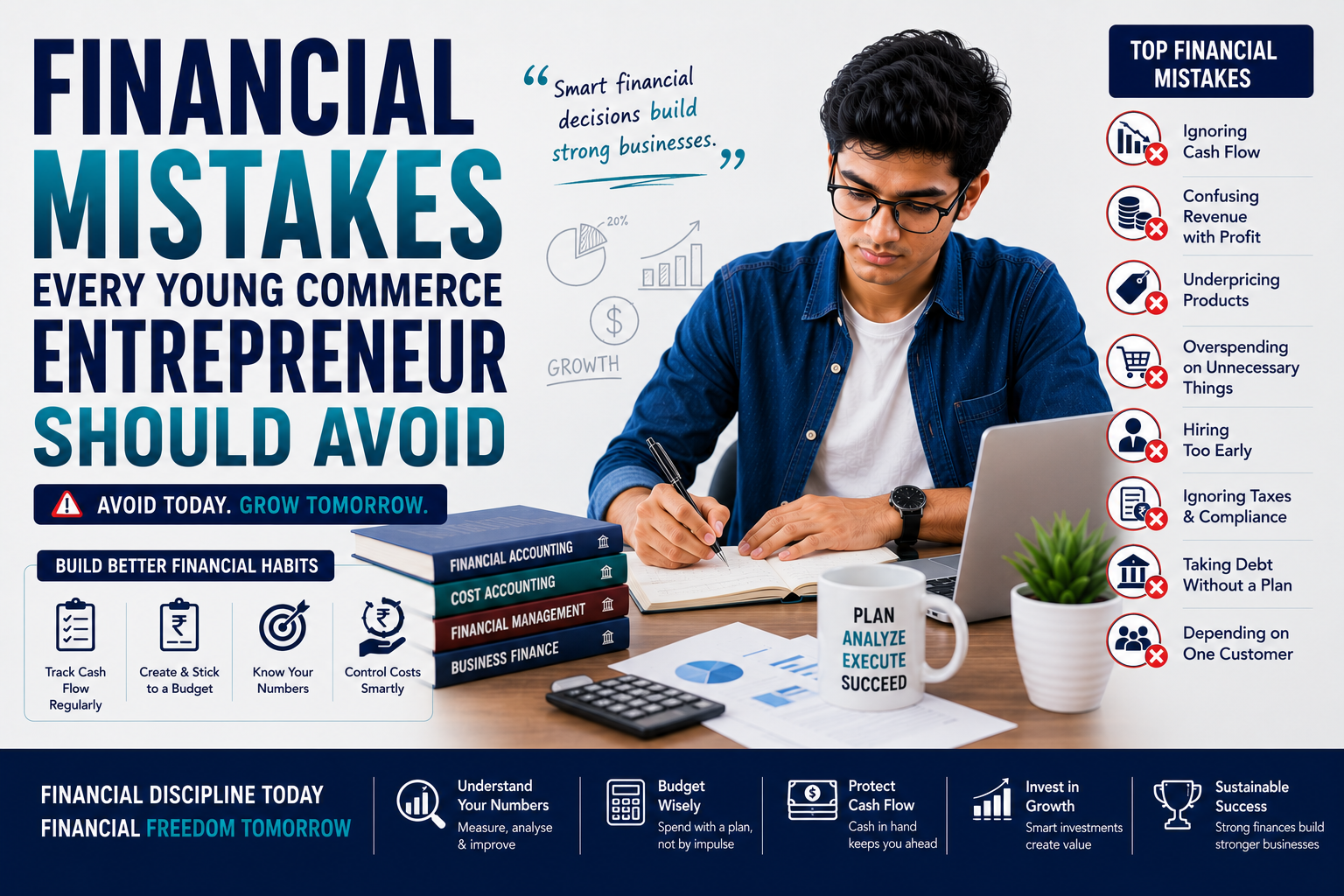

Financial Mistakes Every Young Commerce Entrepreneur Should Avoid?

Commerce students often enter entrepreneurship with an advantage.

They understand accounting basics. Many have studied costing, taxation, economics and financial management. CA and CMA students may have even deeper technical knowledge.

So, they shouldn’t make financial mistakes in business. Right?

Not exactly.

Knowing a concept for an exam and applying it when your own money is at risk are two very different experiences.

A student may know how to prepare a cash flow statement but still forget to monitor the startup’s bank balance every week. Someone may understand cost accounting yet price a product emotionally because they desperately want customers.

Real business decisions are messy.

There are employees waiting for salaries, customers asking for discounts, suppliers demanding payment and competitors cutting prices.

This is why startup financial mistakes happen even when founders have studied commerce.

The good news is that many of these mistakes are predictable.

And preventable.

Why Financial Mistakes Hurt Startups So Quickly?

Large companies usually have finance departments, established systems and access to capital.

Young businesses don’t always have those advantages.

A small mistake can quickly become a serious problem.

Consider a startup with ₹10 lakh in cash.

An unnecessary ₹1 lakh expense consumes 10% of its available money.

For a company holding ₹100 crore in cash, the same ₹1 lakh mistake may barely be noticed.

That’s why young entrepreneurs must be careful with capital.

Every rupee doesn’t need to be protected obsessively. Businesses must spend to grow.

But founders should understand why money is being spent and what the business expects in return.

1. Confusing Revenue with Profit

This is one of the oldest business mistakes.

And it still happens.

A founder proudly says:

“We did ₹50 lakh in sales this year.”

That’s useful information.

But it doesn’t tell us whether the business made money.

Suppose the numbers look like this:

| Financial Item | Amount |

|---|---|

| Revenue | ₹50 lakh |

| Product Costs | ₹25 lakh |

| Marketing | ₹10 lakh |

| Salaries | ₹12 lakh |

| Other Expenses | ₹5 lakh |

| Total Expenses | ₹52 lakh |

The company generated ₹50 lakh in revenue.

It also spent ₹52 lakh.

Revenue is impressive.

Profitability tells a different story.

Young entrepreneurs should regularly monitor gross profit, operating expenses and net profit instead of celebrating sales alone.

2. Ignoring Cash Flow

A profitable business can still run out of cash.

This surprises many first-time entrepreneurs.

Imagine a startup sells services worth ₹20 lakh to corporate customers.

The invoices are recorded.

Revenue looks healthy.

But customers pay after 90 days.

Meanwhile, the company must pay salaries and vendors every month.

The result?

A cash shortage.

Founders should monitor:

- Bank balance

- Expected customer payments

- Supplier payments

- Salary obligations

- Loan repayments

- Tax liabilities

A simple 13-week cash flow forecast can help businesses identify potential shortages before they become emergencies.

Practical note: profit is important. Cash decides whether you can pay Friday’s bills.

3. Mixing Personal and Business Money

This often begins innocently.

A founder pays a business bill from a personal account.

Then uses the company card for a personal purchase.

Later, money moves between accounts without clear documentation.

Within months, nobody knows exactly what belongs to the founder and what belongs to the business.

Maintain separate financial records and appropriate banking arrangements for the business based on its legal structure.

Clear separation makes:

- Accounting easier

- Expense tracking clearer

- Tax preparation more organised

- Financial analysis more reliable

Treat your startup like a real business from Day One.

Even if you’re the only employee.

4. Starting Without a Financial Budget

Many young founders prepare a business idea.

Some prepare a pitch deck.

Very few prepare a detailed operating budget.

That’s a mistake.

Before starting, estimate expenses such as:

- Product development

- Salaries

- Rent

- Technology

- Marketing

- Professional fees

- Compliance costs

- Working capital

Your budget won’t be perfectly accurate.

It doesn’t need to be.

The goal is to understand how much money the business may require.

A rough financial plan is better than discovering six months later that you underestimated expenses by 50%.

5. Underpricing Products to Attract Customers

Young entrepreneurs often believe low prices are the easiest way to win customers.

Sometimes they are.

But low pricing can create a dangerous business model.

Suppose a product sells for ₹1,000.

The direct product cost is ₹500.

The founder sees a ₹500 margin.

Then reality arrives.

There is a ₹150 advertising cost.

₹70 shipping.

₹30 payment processing.

₹100 allocated to customer support and overheads.

The apparent ₹500 margin has almost disappeared.

Before setting a price, understand the complete cost structure.

Cheap doesn’t automatically mean competitive.

Sometimes it simply means unprofitable.

6. Spending Too Much on Office and Appearance

A beautiful office feels like progress.

Expensive furniture feels professional.

A large team creates the appearance of growth.

But appearance doesn’t always create revenue.

Early-stage entrepreneurs sometimes spend heavily on:

- Premium offices

- Expensive interiors

- Unnecessary equipment

- Luxury business travel

- Branding before product validation

Some of these investments may eventually be necessary.

Timing matters.

Ask a simple question before major spending:

Does this expense improve the product, customer experience, operations or revenue potential?

If the answer is unclear, wait.

7. Hiring Too Early

Hiring is one of the largest financial commitments a startup makes.

An employee’s cost isn’t limited to monthly salary.

Businesses may also incur costs related to:

- Recruitment

- Equipment

- Software

- Training

- Workspace

- Employee benefits

Founders sometimes hire because they feel busy.

Busy doesn’t always mean you need a full-time employee.

Before hiring, ask:

- Is this workload permanent?

- Can the process be automated?

- Can it be outsourced temporarily?

- Will this role directly support growth or operations?

- Can the company afford the employee for the next 12 months?

Hire for a clear business need.

Not because having a larger team looks impressive on LinkedIn.

8. Failing to Track Receivables

A sale isn’t useful if the customer never pays.

B2B businesses must pay particular attention to accounts receivable.

Consider this situation.

A startup has ₹30 lakh in outstanding invoices.

The founder assumes the company is financially strong.

But ₹15 lakh is overdue by more than 120 days.

That’s a warning sign.

Track:

- Invoice date

- Payment due date

- Amount outstanding

- Days overdue

- Customer payment history

Follow up systematically.

Revenue quality matters.

9. Taking Debt Without Understanding Repayment Pressure

Business loans can support growth.

They can also create financial pressure.

Before borrowing, founders should understand:

- Interest rate

- Repayment schedule

- Loan tenure

- Security or guarantees

- Cash flow impact

- Consequences of delayed payments

A loan should ideally support a clear business purpose.

Borrowing to fund productive assets or working capital may make sense depending on the business.

Borrowing simply to cover repeated operating losses deserves closer examination.

Debt doesn’t fix a weak business model.

Sometimes it only delays the problem.

10. Raising Investment Without Understanding Dilution

Startup funding often receives glamorous media coverage.

“Startup raises ₹50 crore.”

What receives less attention?

Ownership dilution.

When founders raise equity investment, they generally exchange part of the company’s ownership for capital.

Suppose founders own 100% of a company.

After multiple funding rounds, their ownership percentage may reduce significantly.

This isn’t automatically bad.

Owning 20% of a highly valuable company can be better than owning 100% of a struggling business.

But founders should understand:

- Valuation

- Equity dilution

- Cap tables

- Investor rights

- Funding terms

Never celebrate the funding amount without understanding the deal structure.

11. Ignoring Unit Economics

A startup can grow quickly and become financially weaker at the same time.

Sounds impossible?

Imagine a company loses ₹100 on every order.

At 1,000 orders, the loss related to those unit economics is ₹1 lakh.

At 100,000 orders, the problem becomes much larger.

More sales don’t always solve weak economics.

Depending on the business model, founders should understand metrics such as:

- Contribution margin

- Customer Acquisition Cost (CAC)

- Customer Lifetime Value (LTV)

- Average Revenue Per User (ARPU)

- Churn rate

The specific metrics vary by industry.

The principle doesn’t.

Understand the economics of your core business activity.

12. Growing Faster Than the Business Can Support

Growth is exciting.

A second branch.

A new city.

More employees.

A bigger marketing campaign.

But rapid expansion increases financial requirements.

A retail company opening five branches may need money for:

- Deposits

- Interiors

- Inventory

- Staff

- Marketing

- Working capital

Revenue from those branches may take months to stabilise.

Growth consumes cash before it produces cash in many businesses.

This is why founders should build financial forecasts before major expansion.

Ask:

What happens if the new branch takes twice as long to break even?

That’s not negativity.

That’s financial planning.

13. Forgetting About Taxes and Compliance

Young founders often focus entirely on sales.

Tax gets attention only when a deadline approaches.

Depending on the business and applicable regulations, financial obligations may involve areas such as GST, income tax, TDS and corporate filings.

The exact requirements depend on the company’s legal structure and activities.

Professional advice from a qualified expert may be necessary.

Founders should still maintain organised records and understand upcoming financial obligations.

Tax money isn’t extra business cash.

Don’t spend it as if it is.

14. Not Maintaining an Emergency Cash Buffer

Businesses face surprises.

A major customer delays payment.

Equipment fails.

Sales temporarily fall.

A supplier increases prices.

Without cash reserves, small problems become serious crises.

There is no universal emergency cash amount that works for every business.

The appropriate buffer depends on:

- Fixed expenses

- Revenue stability

- Industry

- Debt obligations

- Customer concentration

Founders should assess their financial risk and maintain appropriate liquidity where possible.

15. Depending on One Major Customer

Imagine one customer contributes 70% of a startup’s revenue.

Everything looks excellent.

Until that customer leaves.

Customer concentration creates financial risk.

A founder should regularly analyse how much revenue comes from the largest customers.

If one client dominates the business, develop a strategy to diversify revenue.

Don’t wait until the cancellation email arrives.

16. Making Financial Decisions Emotionally

Entrepreneurship is emotional.

Founders become attached to products, employees and ideas.

Finance requires occasional distance.

A founder may continue funding an unsuccessful product because:

“We’ve already spent ₹20 lakh.”

But money already spent is a sunk cost.

The better question is:

Based on what we know today, should we continue investing?

Past spending shouldn’t automatically justify future spending.

CA and CMA students study decision-making concepts like relevant costs and sunk costs.

Entrepreneurs experience them in real life.

17. Not Reviewing Financial Numbers Regularly

Some founders review financial statements only once a year.

That’s far too late for a young business.

You don’t need a complicated dashboard containing 100 metrics.

Start with a small financial review.

Depending on the business, monitor:

| Metric | Why It Matters |

|---|---|

| Cash Balance | Shows immediate liquidity |

| Revenue | Tracks sales activity |

| Gross Margin | Measures core economics |

| Operating Expenses | Identifies spending trends |

| Receivables | Tracks customer payments |

| Cash Burn | Shows cash consumption |

| Runway | Estimates financial survival period |

Review frequency depends on the company.

Cash may need weekly attention.

Broader financial performance may be reviewed monthly.

The key is consistency.

A Simple Financial Checklist for Young Entrepreneurs

Before making a major financial decision, ask:

- How much will this cost?

- Can the business afford it?

- What financial result do we expect?

- When might we see that result?

- What happens if the plan fails?

- Does this affect cash flow?

- Are there tax or compliance implications?

- Can we test the idea on a smaller scale first?

Eight questions.

They can prevent surprisingly expensive mistakes.

What CA & CMA Students Can Learn from Startup Financial Mistakes?

Commerce students shouldn’t wait until they launch a business to learn these lessons.

Study real companies.

Analyse why businesses struggle.

Build simple financial models.

Read annual reports.

Study startup economics.

Take a small imaginary business and calculate:

- Revenue

- Gross margin

- Monthly expenses

- Break-even point

- Cash requirement

- Funding need

The goal is to develop financial judgement.

Exams test whether you know the concept.

Business tests whether you know when to use it.

Frequently Asked Questions

What are the most common startup financial mistakes?

Common mistakes include ignoring cash flow, confusing revenue with profit, underpricing products, overspending, hiring too early and failing to track receivables.

Why do startups fail because of financial problems?

Startups may face cash shortages, weak unit economics, excessive costs, poor pricing or uncontrolled growth. Financial problems can become serious quickly when capital is limited.

How can entrepreneurs avoid cash flow problems?

Entrepreneurs can regularly track cash inflows and outflows, monitor receivables, forecast upcoming payments and maintain appropriate cash reserves.

Is revenue more important than profit for startups?

Revenue is an important growth indicator, but founders should also understand profitability, cash flow and unit economics. The right priorities can vary by startup stage and business model.

Why is budgeting important for startups?

Budgeting helps founders allocate limited capital, plan expenses and compare actual spending with expectations.

Should startups take business loans?

Debt may be useful in certain situations, but founders should understand repayment obligations, interest costs and cash flow impact before borrowing.

How can commerce students learn from startup financial mistakes?

Commerce students can study real businesses, build financial models, analyse cash flow, calculate break-even points and apply accounting and finance concepts to practical business situations.